Understanding SIL Pricing Dynamics: Why Status Quo will Persist

- Want to get in touch?

Dean Bowman

December 3, 2025

As the disability sector continues advocating for SIL price increases, it’s worth examining the economic and political dynamics that shape pricing decisions. This analysis explores what policymakers likely observe in the data, the constraints they face, and why the path to price increases may be steeper than many anticipate.

National Cabinet established an 8% annual growth target for NDIS expenditure in June 2023, with government projecting $14.4 billion in savings over four years from July 2024. This creates a binding fiscal constraint that shapes all pricing discussions. Facing such constraints, policymakers cannot rely primarily on provider sentiment, however legitimate, to justify significant expenditure increases. While survey data showing 81% of providers concerned about pricing viability provides important context, it presents challenges as a decision-making foundation: sentiment is subjective, reflects aggregate concerns across diverse service lines, and doesn’t differentiate between calls for margin improvement versus genuine market failure.

Instead, governments facing fiscal constraints tend to rely on objective metrics that provide verifiable signals of market health. Three metrics stand out as particularly useful for pricing decisions:

These metrics offer something sentiment cannot: objective, quantifiable evidence of whether markets are clearing efficiently or experiencing dysfunction requiring intervention.

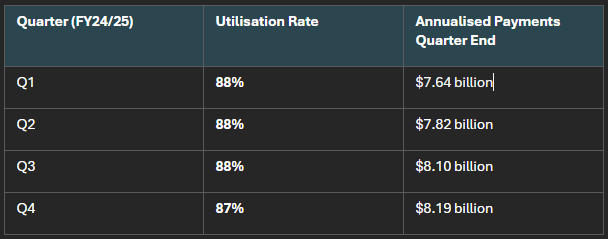

The current SIL utilisation data tells a specific story:

Quarter (FY24/25) | Utilisation Rate | Annualised Payments Quarter End |

Q1 | 88% | $7.64 billion |

Q2 | 88% | $7.82 billion |

Q3 | 88% | $8.10 billion |

Q4 | 87% | $8.19 billion |

Utilisation rates of 87-88% are remarkably high and stable. This consistency across four quarters suggests participants are accessing services, providers are delivering supports, and the market is clearing efficiently at current price levels.

From a policy perspective, 87-88% utilisation represents what efficient markets look like: not too low to signal dysfunction, not so high as to suggest inadequate funding, but in the zone where supply and demand meet effectively.

Compare this to therapy supports, which experienced price freezes for four consecutive years and had travel/access components reduced despite provider advocacy. Therapy supports had utilisation rates below 70%, before the recent pricing intervention. This example demonstrates that treasury likely understand utilisation is an important fiscal tool, and that markets with relatively poor utilisation are still subject to downward market intervention. This places SIL’s utilisation rate firmly outside of the band where one could expect pricing action.

The combination of high utilisation and rapid spending growth tells an important story about supply dynamics:

Year | Participants | Total Payments ($M) | Avg Payment |

2022 | 28,018 | $9,222 | $347,700 |

2023 | 32,973 | $12,254 | $397,900 |

2024 | 35,371 | $14,463 | $422,300 |

2025 | 36,641 | $15,896 | $438,200 |

Growth 2022-2025 | +31% | +72% | +26% |

When spending grows by 72% while utilisation remains constant at 87-88%, it reveals that budgeted/allocated funds are growing substantially (more participants, higher plan values) AND participants are successfully accessing services at the same high rate. This means supply is expanding in lockstep with demand. If budgets had grown but utilisation fell, that would signal supply failure, participants couldn’t spend their allocated funds because services weren’t available. But sustained high utilisation alongside spending growth demonstrates the market is successfully scaling capacity to meet expanding budgeted demand.

While survey data shows legitimate provider concerns about operating conditions, actual capital allocation tells a different story. From the NDS data In 2025:

This creates an interesting dynamic from a policy perspective. Providers are simultaneously:

From a government perspective facing fiscal constraints, this gap between stated sentiment and revealed preference through behaviour becomes relevant. Organisations making rational resource allocation decisions are choosing to expand SIL capacity. This suggests, whatever the challenges in other service lines or smaller providers’ experience, that major players see continuing viability in SIL at current pricing.

When providers allocate scarce capital to expand a service line while simultaneously advocating for price increases in that line, it signals the service remains economically viable even if margins aren’t what providers would prefer.

This isn’t to dismiss provider concerns, operating environments are genuinely challenging, and many organisations face real pressures. But it does suggest that there is a substantial segment of the market demonstrating preference falsification with the view of margin optimisation. It is important to note that the SIL market is notoriously quality opaque, and it is unlikely that quality supports will be able to exert a price signal soon. This does unfortunately mean that SIL will continue a rapid race to the bottom unless quality is effectively priced in. Given the lack of any such mechanism on the horizon, our view is that SIL will continue to behave like a commodity. Which leads to the next question:

One concern worth addressing: what if major providers exit? The SIL market exhibits remarkably low concentration, which provides inherent resilience:

Metric | Annual Amount |

Top 3 Providers Combined NDIS Revenue | $1,250 million |

Annual SIL Market Expansion | $2,200 million |

Market Expansion as % of Top 3 | 176% |

The annual SIL market expansion ($2.2 billion) is 176% of the top three providers’ combined NDIS revenue. This means that even in the extreme scenario where all three major providers simultaneously exited (which is extraordinarily unlikely) the market’s natural growth would absorb their capacity within approximately seven months.

Moreover, there have been provider exits from the NDIS more broadly, yet the utilisation data shows no disruption. The market absorbed these exits without visible impact on service delivery. This is demonstrated resilience that the NDIA are likely aware of. The sector has already stress-tested its ability to maintain function through provider churn, and the data shows it passed that test.

Gresham’s law stated as “Bad money will drive out good money” is a sort of structural race to the bottom that SIL is current subjected to. Presently, from an outside perspective (such as that of participants purchasing SIL for the first time) there are no reliably quality signals that differentiate one SIL product from another. This is exacerbated by the sheer volume of conflicted intermediaries in the sector (unfortunately, many unconflicted intermediaries have been driven out by price freezing).

In the peculiar case of SIL “bad money” can drive out good money with the following advantages.

With the lack of rigorous enforcement, or a visible service standard for SIL, Gresham’s law will play out to its logical conclusion. Noting that while utilization for SIL is high and funding is expanding, Gresham’s law will also likely prevent the improvement of pricing or SIL structuring. In fact, it may worsen it substantially, noting that any degree of freedom offered to the market may be abused for profit generation.

You can see this pattern for yourself by observing Freedom Care Group’s organic growth rate when contrasted against large incumbents who one would have thought, have significant structural advantages.

It’s worth acknowledging the unique political economy of SIL. Government understands that SIL participants typically require substantial 24/7 care with significant safety considerations. These support needs are documented in NDIA planning decisions and involve vulnerable individuals with complex requirements.

This creates an important constraint: any action that threatens SIL supply would be politically challenging regardless of the economic rationale. This is quite different from other support categories where service interruption, while undesirable, might be less immediately critical. This offers SIL some protection against the perverse incentive of the NDIA, to constrain utilisation to find automatic spending savings. The political constraint means SIL pricing likely sits in a particular equilibrium, it cannot be reduced without risking supply to vulnerable participants, but the market signals don’t create pressure for increases either.

Finally, it’s worth considering the fiscal implications of price increases. Current SIL payments are approximately $8.2 billion:

Against a $14.4 billion four-year savings target, these figures represent substantial proportions of the entire fiscal envelope. Treasury would require compelling evidence of market failure to justify such expenditure. The current signals: high utilisation, expanding supply and provider expansion provide the opposite story.

This analysis suggests that substantial SIL price increases face significant headwinds, not because provider concerns aren’t legitimate, but because the objective market signals don’t indicate the systemic failure that would justify major expenditure increases in a fiscally constrained environment.

For providers, this creates strategic imperatives:

The 60% of organisations now focusing on market research, strategy and planning (up from 28% in 2024) suggests the sector is already recognising these imperatives.

Understanding the signals policymakers likely observe: high utilisation, expanding supply, provider investment, helps clarify why price increases may not materialise despite legitimate provider advocacy. This doesn’t invalidate sector concerns about challenging operating environments. But it does suggest that solutions may lie more in business model adaptation, consolidation for scale, and operational efficiency than in waiting for pricing relief that the market signals suggest is unlikely.

The disability sector has demonstrated remarkable resilience and adaptability throughout the NDIS journey. The next phase may require applying that same resilience to operating within the current pricing environment rather than expecting it to change.

This analysis draws on publicly available data from the National Disability Services State of the Disability Sector Reports (2023-2025), financial statements from major providers, and market utilisation data. It represents an economic analysis of policy incentives and market signals, not an endorsement of any particular policy position.

Join an exclusive community of providers receiving our eNewsletter Empathia Insider. Get first access to NDIS business insights, free provider resources, and special offers direct to your inbox.

Empathia Group is a collective of business consultants focused on creating sustainable, long-term success for NDIS service providers.

Appointments outside of standard business hours available by request

Empathia Group Pty Ltd © 2022. All rights reserved.

How are you?

If you’re looking for a sandbox experience with endless meme potential, nextbots sandbox of memes is a must-play! Its creative freedom and varied features allow for truly unique and hilarious gameplay scenarios. Jump in and start building your own meme-fueled chaos!

A really good blog and me back again.

vzom4w

cwnjc9

7seu2t

每天都在战争,希望2026和平.

hacklink,hacklink panel,hacklink satın al , hacklink,hacklink panel,

hacklink satın al , hacklink,hacklink panel,hacklink satın al

How to propose beautifully private proposal in Barcelona

Hacklink satın almak, web siteni Google’da hızlıca üst sıralara taşımak için etkili bir yöntemdir. Hacklink dediğimiz bağlantılar, sıradan backlinklerden farklı …

уличные навесы где заказать навесы

bu2xzj

Hacklink panel avantajları ile tanışın. Toplu link ekleme, zamanlayıcı özelliği ve özelleştirilebilir kampanya seçenekleri.

Качественное SEO https://outreachseo.ru продвижение сайта для бизнеса. Наши специалисты предлагают эффективные решения для роста позиций в поисковых системах. Подробнее об услугах и стратегиях можно узнать на сайте

bedava bitcoin, ücretsiz kripto, casino bonus,

casino sitesi, güvenilir casino, online casino,

canlı casino, slot oyunları, rulet oyna, poker oyna, blackjack oyna,

bahis sitesi, güvenilir bahis, canlı bahis, spor bahisleri, yüksek oran bahis, kaçak bahis,

bedava bahis, deneme bonusu, hoşgeldin bonusu, casino free spin, slot free spin, kumar

sitesi, kumarhane, çevrimiçi kumar, illegal bahis, yasa dışı

bahis, illegal casino, yasadışı kumar, kayıt olmadan bahis, kimlik doğrulama yok bahis,

bahis para yatır, bahis para çek, casino para çekme,

casino para yatırma, slot jackpot, jackpot casino,

bedava casino, ücretsiz casino, casino demo,

canlı krupiye, canlı rulet, canlı blackjack, canlı poker, canlı baccarat, baccarat

oyna, baccarat sitesi, çevrimsiz bonus, yatırımsız

bonus, çevrim şartsız bonus, kayıp bonusu, kayıp iadesi, free bet, freespin, casino cashback, bahis cashback, bedava iddaa, maç

izle bahis, canlı maç bahis, futbol bahis, basketbol bahis, tenis bahis, esports bahis,

sanal bahis, sanal spor bahis, köpek yarışı bahis, at yarışı bahis, greyhound bahis, poker freeroll, escort bayan, escort istanbul, escort ankara, escort izmir, escort bursa, escort adana, escort kocaeli,

escort mersin, escort antalya, escort gaziantep, escort konya, escort

diyarbakır, escort aydın, escort kayseri, vip escort, ucuz escort, eve gelen escort,

otele gelen escort, saatlik escort, gecelik escort, haftalık escort,

çıkmalık escort, rezidans escort, öğrenci escort,

yabancı escort, rus escort, ukraynalı escort, arap escort, sarışın escort,

esmer escort, olgun escort

bedava bitcoin, ücretsiz kripto, casino bonus, casino sitesi,

güvenilir casino, online casino, canlı casino, slot oyunları, rulet

oyna, poker oyna, blackjack oyna, bahis sitesi, güvenilir bahis, canlı bahis, spor bahisleri, yüksek oran bahis, kaçak bahis, bedava bahis, deneme bonusu, hoşgeldin bonusu, casino free spin, slot free spin, kumar sitesi,

kumarhane, çevrimiçi kumar, illegal bahis, yasa dışı bahis, illegal casino, yasadışı kumar,

kayıt olmadan bahis, kimlik doğrulama yok bahis, bahis para yatır, bahis para çek, casino para

çekme, casino para yatırma, slot jackpot, jackpot

casino, bedava casino, ücretsiz casino, casino demo, canlı krupiye, canlı rulet,

canlı blackjack, canlı poker, canlı baccarat, baccarat oyna, baccarat sitesi, çevrimsiz bonus, yatırımsız

bonus, çevrim şartsız bonus, kayıp bonusu, kayıp iadesi, free bet, freespin, casino cashback, bahis

cashback, bedava iddaa, maç izle bahis, canlı

maç bahis, futbol bahis, basketbol bahis, tenis bahis, esports bahis, sanal bahis,

sanal spor bahis, köpek yarışı bahis, at yarışı bahis,

greyhound bahis, poker freeroll, escort bayan, escort istanbul, escort ankara, escort izmir, escort

bursa, escort adana, escort kocaeli, escort mersin, escort antalya,

escort gaziantep, escort konya, escort diyarbakır, escort aydın, escort kayseri, vip

escort, ucuz escort, eve gelen escort, otele gelen escort, saatlik

escort, gecelik escort, haftalık escort, çıkmalık escort,

rezidans escort, öğrenci escort, yabancı escort,

rus escort, ukraynalı escort, arap escort, sarışın escort, esmer escort, olgun escort

May you always find beauty and joy in the simple things of life

Нужен банный веник? купить веник для бани натуральные банные веники помогают улучшить эффект парения и создать особую атмосферу в бане. У нас можно купить веник для бани из березы, дуба или эвкалипта.

bedava bitcoin, ücretsiz kripto, casino bonus,

casino sitesi, güvenilir casino, online casino, canlı

casino, slot oyunları, rulet oyna, poker oyna, blackjack oyna, bahis sitesi, güvenilir bahis, canlı bahis, spor bahisleri, yüksek oran bahis,

kaçak bahis, bedava bahis, deneme bonusu, hoşgeldin bonusu, casino free spin, slot free spin,

kumar sitesi, kumarhane, çevrimiçi kumar, illegal bahis,

yasa dışı bahis, illegal casino, yasadışı kumar,

kayıt olmadan bahis, kimlik doğrulama yok bahis, bahis para yatır, bahis para çek,

casino para çekme, casino para yatırma, slot jackpot, jackpot casino,

bedava casino, ücretsiz casino, casino demo, canlı krupiye,

canlı rulet, canlı blackjack, canlı poker, canlı baccarat, baccarat oyna, baccarat sitesi, çevrimsiz bonus, yatırımsız

bonus, çevrim şartsız bonus, kayıp bonusu,

kayıp iadesi, free bet, freespin, casino cashback, bahis cashback, bedava iddaa,

maç izle bahis, canlı maç bahis, futbol bahis, basketbol

bahis, tenis bahis, esports bahis, sanal bahis, sanal spor bahis, köpek yarışı bahis, at yarışı bahis, greyhound bahis,

poker freeroll, escort bayan, escort istanbul, escort ankara, escort izmir, escort bursa, escort adana, escort kocaeli, escort mersin, escort

antalya, escort gaziantep, escort konya, escort diyarbakır,

escort aydın, escort kayseri, vip escort, ucuz escort, eve gelen escort, otele gelen escort,

saatlik escort, gecelik escort, haftalık escort, çıkmalık escort, rezidans escort, öğrenci escort,

yabancı escort, rus escort, ukraynalı escort, arap escort, sarışın escort, esmer escort, olgun escort

Нужен банный веник? купить дубовый веник натуральные банные веники помогают улучшить эффект парения и создать особую атмосферу в бане. У нас можно купить веник для бани из березы, дуба или эвкалипта.

Противопожарные двери https://zavod-dverimontazh.moscow от производителя с профессиональной установкой в Москве. Изготовление по ГОСТ, сертифицированные конструкции с высокой огнестойкостью. Металлические противопожарные двери для офисов, складов, жилых и коммерческих зданий. Доставка, монтаж, гарантия качества и выгодные цены.

Любишь азарт? пин ап официальный сайт казино предлагает разнообразные игровые автоматы, настольные игры и интересные бонусные программы. Платформа создана для комфортной игры и предлагает широкий выбор развлечений.

Любишь азарт? https://pfrrt.ru предлагает разнообразные игровые автоматы, настольные игры и интересные бонусные программы. Платформа создана для комфортной игры и предлагает широкий выбор развлечений.

Все о строительстве https://dipris-studio.ru и дизайне загородного дома: современные проекты, идеи планировки, выбор материалов, этапы строительства и оформление интерьера. Полезные советы по строительству коттеджей, ремонту и благоустройству участка. Практические рекомендации для владельцев домов и тех, кто только планирует строительство.

Новостной портал https://newsn.ru — свежие новости России и мира, политика, экономика, общество, технологии и культура. Оперативные публикации, аналитические материалы и главные события дня. Узнавайте важные новости первыми и следите за развитием событий онлайн.

Все о строительстве https://sportdon.ru и ремонтах: рекомендации по выбору материалов, технологиям строительства, отделке помещений и дизайну интерьера. Полезные статьи для тех, кто строит дом, делает ремонт квартиры или планирует обновление интерьера.

Портал про здоровье https://vekneboley.ru с полезными статьями о профилактике заболеваний, правильном питании, иммунитете и здоровом образе жизни. Рекомендации специалистов, советы по поддержанию здоровья, физической активности и улучшению самочувствия каждый день.

Портал новостей https://hand-store.ru о высоких технологиях и IT-индустрии. Последние события в мире программирования, искусственного интеллекта, стартапов, гаджетов и цифровых технологий. Читайте обзоры, аналитические материалы и важные новости технологического рынка.

Портал о бытовой https://expert-byt.ru технике и ее эксплуатации. Полезные статьи о выборе техники для дома, правильном использовании, уходе и продлении срока службы устройств. Советы по ремонту, обслуживанию и эффективному использованию бытовой техники в повседневной жизни.

Читайте свежие новости https://иваново37.рф России на новостном портале. Главные события дня, политика, экономика, общество, технологии и культура. Оперативные публикации, аналитика и важная информация о событиях в стране и мире.

Все о смартфонах https://topse.ru мобильных телефонах и гаджетах Sony. Новости, обзоры новых моделей Xperia, характеристики устройств, сравнение смартфонов и полезные советы по выбору техники. Узнайте о новинках Sony, технологиях камер, производительности и возможностях мобильных устройств.

Свежие мировые https://novostizn.ru новости и интересные события со всех уголков планеты. Политика, экономика, технологии, культура, наука и общественная жизнь. Актуальные новости, аналитика и необычные факты о событиях, которые обсуждает весь мир.

Мировые новости https://dikb.ru и интересные события каждый день. Самые важные события политики, экономики, технологий, науки и культуры. Свежие публикации, аналитика и необычные факты о происходящем в разных странах мира.

Live streams http://www.selcuksport.com.az of football matches and sports TV shows online. Football news, schedules, results, and analysis. Follow your favorite teams, watch highlights, and stay up-to-date on the latest news from the world of football.

Противопожарные двери https://zavod-dverimontazh.moscow в Москве от производителя. Надежные металлические двери с высокой огнестойкостью для жилых и коммерческих помещений. Сертификация, соответствие нормам пожарной безопасности, быстрая доставка и установка противопожарных дверей под ключ.

Playmods APK playmods com az is a convenient app for downloading modified games and apps on Android. It offers a large catalog of popular games, fast mod updates, additional features, and a simple interface for easy searching and installation.

Наша лучшая подборка: https://perfumerio.ru/s/carner-barcelona-besos/

Общаешься в максе? приложение макс мессенджер удобный способ найти интересные каналы в мессенджере. Новости, технологии, бизнес, развлечения и другие категории. Просматривайте популярные каналы, открывайте новые источники информации и подписывайтесь.

Консультация семейного юриста поможет быстро разобраться в сложных жизненных ситуациях: развод, раздел имущества, алименты, споры о детях и брачные договоры. Перейдя по запросу юристы по семейным жилищным вопросам – специалист объяснит ваши права, оценит перспективы дела и предложит оптимальный план действий. Получите профессиональную юридическую помощь и ответы на все вопросы по семейному праву.

Строительный портал https://apis-togo.org с полезными статьями о строительстве домов, ремонте квартир и выборе строительных материалов. Советы специалистов, современные технологии строительства, идеи дизайна интерьера и практические рекомендации для ремонта и обустройства жилья.

Строительный журнал https://eeu-a.kiev.ua о строительстве, ремонте и дизайне. Полезные статьи о строительных технологиях, выборе материалов, отделке помещений и обустройстве дома. Практические советы для тех, кто строит дом или делает ремонт.

Строительный портал https://furbero.com с полезной информацией о строительстве домов, ремонте квартир и отделке помещений. Советы по выбору материалов, современные технологии строительства и идеи дизайна интерьера для комфортного жилья.

Все о строительстве https://elektrod.com.ua и ремонте на строительном портале. Советы по выбору строительных материалов, технологиям строительства, отделке помещений и дизайну интерьера. Полезные рекомендации для владельцев домов, квартир и загородной недвижимости.

Полезные статьи https://novostroi.in.ua о строительстве и ремонте на строительном портале. Технологии строительства, выбор материалов, отделка помещений и дизайн интерьера. Практические рекомендации для строительства дома и ремонта квартиры.

Портал про автомобили https://carexpert.com.ua новости автоиндустрии, обзоры новых моделей, тест-драйвы и советы по эксплуатации машин. Полезные статьи для автолюбителей о выборе автомобиля, ремонте, обслуживании и современных автомобильных технологиях.

Автомобильный портал https://autoiceny.com.ua для автолюбителей. Свежие новости автоиндустрии, обзоры автомобилей, тест-драйвы, рекомендации по эксплуатации и обслуживанию машин. Полезная информация о современных автомобилях и автомобильных технологиях.

Все об автомобилях https://eurasiamobilechallenge.com на автомобильном портале. Новости автоиндустрии, обзоры машин, тест-драйвы, советы по ремонту и обслуживанию автомобилей. Узнайте о новых моделях авто, технологиях и событиях автомобильного рынка.

Портал о строительстве https://proektsam.kyiv.ua и ремонте домов и квартир. Полезные статьи о строительных технологиях, выборе материалов, отделке помещений и дизайне интерьера. Советы специалистов и практические рекомендации для обустройства жилья.

Автомобильный портал https://mallex.info с новостями автоиндустрии, обзорами автомобилей, тест-драйвами и полезными советами для водителей. Узнайте о новых моделях машин, технологиях автопроизводителей, обслуживании авто и последних событиях автомобильного рынка.

Информационный женский https://gorod-lubvi.com.ua портал о красоте, здоровье, моде, семье и отношениях. Полезные советы, идеи стиля, рецепты, психология и рекомендации для современной женщины. Узнайте, как заботиться о себе и создавать гармонию в жизни.

Женский сайт https://entertainment.com.ua с полезными статьями о красоте, здоровье, моде, отношениях и саморазвитии. Советы по уходу за собой, идеи стиля, рецепты, психология и вдохновение для современной женщины. Читайте интересные материалы и находите полезные советы для повседневной жизни.

Все для женщин https://novaya.com.ua на одном сайте: мода, красота, здоровье, отношения и семья. Полезные советы по уходу за собой, идеи стиля, рецепты и вдохновляющие статьи для современной женщины.

Женский портал https://happytime.in.ua с полезными статьями о моде, красоте, здоровье, отношениях и семье. Советы по уходу за собой, рецепты, идеи стиля и вдохновение для женщин. Все самое интересное и полезное для современной женщины.

Сайт для женщин https://leif.com.ua с полезными советами о красоте, здоровье, моде и отношениях. Статьи о саморазвитии, семье, стиле жизни и уходе за собой. Узнайте секреты женской красоты и гармонии.

Женский сайт https://martime.com.ua о красоте, здоровье, моде и стиле жизни. Советы по уходу за собой, психология отношений, рецепты и полезные рекомендации для современной женщины. Читайте интересные статьи и вдохновляйтесь.

Все о строительстве https://sevgr.org.ua домов, ремонте квартир и благоустройстве жилья на строительном портале. Полезные статьи, рекомендации специалистов, современные технологии строительства и практические советы по выбору строительных материалов и отделке помещений.

Женский портал https://olive.kiev.ua о моде, красоте и здоровье. Полезные советы, рецепты, психология отношений и идеи стиля. Читайте интересные статьи и находите вдохновение для повседневной жизни.

Сайт для женщин https://tiamo.rv.ua с полезными статьями о красоте, здоровье, моде, семье и отношениях. Рекомендации по уходу за собой, идеи стиля, рецепты и советы для гармоничной жизни.

ремонт совмещенного санузла бюджетный ремонт в ванной

Хотите, чтобы ваш профиль или группа в Одноклассниках росли быстрее? Перейдя по запросу сколько стоит накрутка подписчиков в одноклассники вы сможете увеличить количество подписчиков и активность на странице. Чем больше подписчиков — тем выше доверие и интерес к вашему аккаунту. Начните развивать свою страницу уже сегодня!

You ought to be a part of a contest for one of the highest

quality blogs on the web. I’m going to recommend this website!

Сайт новостей https://antifa-action.org.ua Украины и мира с актуальными событиями политики, экономики, общества и технологий. Читайте свежие новости, аналитические материалы и комментарии экспертов. Все главные события Украины и международной повестки.

Актуальные новости https://kiev-online.com.ua Украины и мира на новостном портале. Политика, экономика, общество, технологии и культура. Свежие события, аналитика и важные новости дня.

Информационный сайт https://mediashare.com.ua новостей Украины и мира. Свежие события политики, экономики, общества и технологий. Главные новости дня, аналитика и комментарии экспертов.

Читайте последние https://kiev-pravda.kiev.ua новости Украины и мира на новостном сайте. Политика, экономика, общество, технологии, культура и происшествия. Оперативные обновления и аналитические материалы.

Свежие новости https://actualnews.kyiv.ua Украины и мира на информационном новостном сайте. Политика, экономика, общество, технологии, культура и происшествия. Оперативные публикации, аналитика и комментарии экспертов. Узнавайте главные события дня и следите за развитием новостей.

Сайт о гипертонии https://gipertoniya.net и повышенном артериальном давлении. Полезные статьи о причинах гипертонии, симптомах, профилактике и современных методах лечения. Советы врачей, рекомендации по питанию, образу жизни и контролю артериального давления.

Портал для женщин https://fotky.com.ua с интересными статьями о моде, красоте, здоровье, семье и отношениях. Полезные советы, рецепты, психология отношений и идеи стиля.

Сайт о финансах https://manorsgroup.com.ua и недвижимости с полезными статьями о инвестициях, покупке и продаже недвижимости, ипотеке и управлении личными финансами. Аналитика рынка, советы экспертов и актуальные новости для тех, кто интересуется финансовыми решениями и недвижимостью.

Строительный сайт https://ko-online.com.ua с полезными статьями о строительстве домов, ремонте квартир и выборе строительных материалов. Современные технологии строительства, советы специалистов, идеи дизайна интерьера и практические рекомендации для ремонта и обустройства жилья.

Медицинский портал https://lpl.org.ua с полезными статьями о здоровье, профилактике заболеваний и современных методах лечения. Советы врачей, рекомендации по правильному питанию, укреплению иммунитета и здоровому образу жизни.

Онлайн журнал https://mts-agro.com.ua о садоводстве и дизайне участка. Советы по выращиванию растений, уходу за садом, ландшафтному дизайну и обустройству дачного участка. Идеи для сада, рекомендации по посадке цветов, деревьев и созданию красивого и уютного пространства.

Все о строительстве https://mia.km.ua и ремонте на одном сайте. Полезные советы по выбору строительных материалов, технологиям строительства, отделке помещений и дизайну интерьера. Практические рекомендации для тех, кто строит дом или делает ремонт.

Новостной портал https://sevsovet.com.ua с актуальными новостями Украины и мира. Политика, экономика, общество, технологии и культура. Оперативные новости и аналитические материалы.

Женский портал https://socvirus.com.ua о моде, красоте и здоровье. Полезные советы по уходу за собой, психология отношений, идеи стиля и рекомендации по здоровому образу жизни.

Фитнес-портал https://sportinvent.com.ua о тренировках, здоровом образе жизни и правильном питании. Программы тренировок, советы тренеров, упражнения для дома и зала, рекомендации по похудению и набору мышечной массы. Узнайте, как улучшить физическую форму и поддерживать здоровье.

Хотите быстро развить канал на Rutube? Накрутка подписчиков Rutube поможет увеличить аудиторию, повысить доверие к каналу и ускорить продвижение видео. Перейдя по запросу накрутка просмотров рутуб кворк вы получите живых подписчиков, плавное добавление и безопасные методы продвижения. Отличное решение для новых и развивающихся каналов, которым важно быстрее набрать активность и привлечь больше просмотров. Начните рост канала уже сегодня.

Статьи о маркетинге https://reklamspilka.org.ua PR и рекламе для бизнеса и специалистов. Практические рекомендации по продвижению брендов, управлению репутацией, контент-стратегии, рекламе в интернете и эффективным коммуникациям с клиентами.

Сайт новостей https://vestionline.com.ua Украины и мира с ежедневными обновлениями. Политика, экономика, общество, технологии и культура. Узнавайте последние события и следите за новостями.

Женский интернет-портал https://ledis.top о красоте, здоровье, моде и стиле жизни. Советы по уходу за собой, психология отношений, рецепты и полезные статьи для современной женщины.

Мастерская креативных идей https://rusproekt.org изготовление авторской мебели и текстиля, создание уникального декора и фитодизайна. Отделочные работы в стиле кантри и прованс, оформление интерьеров и индивидуальные дизайнерские решения для дома, кафе и загородных пространств.

Свежие новости https://zoobonus.com.ua Украины и мира в одном месте. Политика, экономика, общество, технологии, культура и происшествия. Актуальные события и аналитические материалы.

Спортивный журнал https://beachsoccer.com.ua о мире спорта. Новости спортивных событий, обзоры матчей, аналитика соревнований и интервью со спортсменами. Читайте актуальные статьи о футболе, хоккее, теннисе, боксе и других популярных видах спорта.

Портал о здоровье глаз https://eyecenter.com.ua и зрении человека. Советы по профилактике заболеваний глаз, улучшению зрения, правильной работе за компьютером и уходу за глазами. Полезные статьи о здоровье глаз и современных методах коррекции зрения.

Чайный портал https://etea.com.ua для любителей чая. Статьи о разных сортах чая, традициях чаепития, способах заваривания и пользе чая для здоровья. Узнайте больше о культуре чая, популярных напитках и интересных фактах о чае.

Портал о технологиях https://helikon.com.ua и инновациях: новости IT, обзоры гаджетов, смартфонов и компьютеров. Статьи о цифровых сервисах, искусственном интеллекте и технологических трендах.

Журнал о строительстве https://bms-soft.com.ua и ремонте для дома и квартиры. Полезные статьи о строительных технологиях, отделке помещений, выборе материалов и ремонте. Советы специалистов, идеи для интерьера и практические рекомендации.

Накрутка подписчиков Rutube поможет быстро увеличить аудиторию канала и повысить доверие к контенту. Живые подписчики создают активность, улучшают видимость роликов и привлекают новых зрителей. Перейдя по запросу накрутить подписчиков на рутуб канал вы получите быстрый старт канала, безопасные методы продвижения и стабильный рост аудитории без отписок. Отличное решение для тех, кто хочет быстрее развить канал на Rutube.

Женский портал https://psilocybe-larvae.com о красоте, здоровье, отношениях и саморазвитии. Полезные советы для женщин, идеи для дома и семьи, мода, психология, рецепты, лайфхаки и вдохновение на каждый день. Читайте статьи, находите полезную информацию и улучшайте свою жизнь.

Мужской портал https://hooligans.org.ua о стиле жизни, здоровье, карьере и саморазвитии. Статьи о спорте, отношениях, финансах, технологиях и мужских интересах. Полезные советы, лайфхаки и вдохновение для современных мужчин.

Информационный автожурнал https://real-voice.info о мире автомобилей. Новости автопрома, обзоры новых моделей, тест-драйвы, сравнения машин, советы по эксплуатации и обслуживанию. Полезные материалы для автолюбителей, владельцев авто и тех, кто выбирает автомобиль.

нужен биг бэг? https://big-bag-mkr.ru: прочные биг-бэги для стройматериалов, зерна, гранулята и других сыпучих продуктов. Производство под заказ и со склада, консультация, расчет, доставка по РФ.

hire car montenegro https://www.montenegro-car-rental-hire.com

Justin TV Azerbaijan https://justin-tv.com.az main page: live match watch, football, big matches, basketball, UFC and game schedule sections.

Продажа квартир https://kvartira778.ru в Санкт-Петербурге от собственников и агентств недвижимости. Актуальные объявления о продаже квартир в новостройках и на вторичном рынке.

Lamine Yamal https://www.lamine-yamal.com.az Barcelona career, statistics, age, where he is from and basic biographical facts. Lamine Yamal profile on one page.

Продажа квартир https://nedvizhkavspb.ru в Санкт-Петербурге. Большой выбор недвижимости на первичном и вторичном рынке: студии, однокомнатные, двухкомнатные и просторные квартиры в разных районах города. Актуальные предложения, удобный поиск и помощь в покупке жилья.

Продвигайте свой аккаунт быстрее с помощью накрутки подписчиков в TikTok. Перейдя по запросу реальные подписчики тик ток Кворк вы сможете увеличить количество фолловеров, повысить доверие к профилю и привлечь больше просмотров и лайков. Быстрая и безопасная накрутка поможет вашему контенту попасть в рекомендации и ускорить рост аккаунта. Подходит для блогеров, брендов и бизнеса, которые хотят развиваться в TikTok и получать больше охватов.

Hacklink panel avantajları ile tanışın. Toplu link ekleme, zamanlayıcı özelliği ve özelleştirilebilir kampanya seçenekleri. 5078

детский стоматолог https://lechenie-zubov-detyam.ru

ремонт ванна комната ремонт ванной комнаты под ключ

Бесплатная консультация семейного юриста — это возможность быстро разобраться в сложной ситуации и понять свои права. Перейдя по запросу адвокат по браку юрист поможет вам по вопросам развода, алиментов, раздела имущества, опеки над детьми и другим семейным спорам. Разъясним перспективы дела и подскажем оптимальное решение. Получите профессиональную помощь без оплаты и лишних обязательств.

Бесплатная консультация юриста по расторжению брака поможет разобраться в ваших правах и возможностях при разводе. Специалист объяснит порядок развода через суд или ЗАГС, подскажет, как решаются вопросы раздела имущества, алиментов и проживания детей. Перейдя по запросу цены на адвоката по разводам в Москве вы получите профессиональные рекомендации и ответы на все вопросы, чтобы пройти процедуру развода максимально спокойно и с защитой ваших интересов.

ремонта ванной комнате ключ https://remont-vannoy-spb.ru

Need a multimedia system? equipment for conference halls We integrate multimedia systems for home and business. We install and configure audio and video systems, manage content, and integrate equipment into a single system. Modern solutions for comfortable and efficient use of technology.

Greetings, There’s no doubt that your website might be having internet browser compatibility

problems. Whenever I take a look at your site in Safari, it looks fine however when opening in IE, it has some overlapping issues.

I simply wanted to give you a quick heads up!

Besides that, excellent blog!

Юридическая консультация по разделу имущества поможет защитить ваши права и избежать ошибок при разводе или спорах между собственниками. Переходите по запросу юридические услуги по разделу бизнеса – юрист оценит ситуацию, разъяснит перспективы дела, подскажет, как правильно оформить документы и выстроить стратегию. Вы получите чёткий план действий и поддержку на каждом этапе — от переговоров до суда.

Все лучшее здесь: https://aromatmasla.ru/bergamot/sochetanie-bergamota.html

Хочешь казино бонус? https://t.me/s/casino_bonus_bezdep/25 всегда актуальные бонусы в онлайн казино. Получайте бонусы без вложений, фриспины и подарки за регистрацию. Актуальные предложения, честные условия отыгрыша и список проверенных казино с бонусами без депозита.

Лучшие казино казино на реальные деньги через сбп: актуальный список онлайн казино с высоким рейтингом, быстрым выводом средств и выгодными бонусами. Обзор лицензий, игр и платежных методов поможет выбрать надежное казино для комфортной игры.

Халява казино рейтинг казино с бонусами за регистрацию: фриспины за регистрацию, бонусы без пополнения и акции для новых игроков. Сравнивайте условия отыгрыша, выбирайте проверенные онлайн казино и начинайте играть бесплатно с возможностью вывода выигрыша.

Лучшие фриспины 2026 бездепозитные фриспины: бесплатные вращения в онлайн казино без вложений. Подборка проверенных сайтов, бонусы за регистрацию, честные условия отыгрыша и возможность вывода выигрыша без риска для игроков.

Официальный сайт покерок скачать: регистрация, вход, бонусы и игра в онлайн покер. Обзор возможностей, турниров, кеш-столов и мобильного приложения. Узнайте, как начать играть и выводить деньги на проверенной платформе.

Every buyer read more should decode VIN number before purchasing any used vehicle.

Every buyer check vin number should check VIN history to confirm clean title and no major accidents.

Luxury travelers https://www.privatejetcharterfly.com choose charter flights for privacy comfort and schedule flexibility.

Transparent pricing https://rentprivatejetfly.com helps you understand exactly how much a private jet costs per flight.

Нужен дизайн участка? ландшафтный дизайн дачного участка проектирование и благоустройство участка с учетом рельефа, растений и стиля. Создаем красивые и функциональные решения для частных домов и дач, подбираем материалы и обеспечиваем качественную реализацию проекта.

Брендирование сувениров https://4youcreation.kz/tisnenie/ в Алматы по современным технологиям. Специалисты предлагают лазерную гравировку, УФ-печать и термоперенос на ткани, стекло, металл и пластик. Организуют доставку по всему Казахстану.

Компания FarbWood https://farbwood.by предлагает пиломатериалы из сибирской лиственницы для частного и коммерческого строительства в Минске и по всей территории Минска. Мы работаем только с лиственницей сибирской, сосна и ель используются как дополнение к основному ассортименту древесины.

Нужна накрутка соц сетей? накрутка просмотров тг увеличение подписчиков, лайков и просмотров для продвижения аккаунтов. Быстрый старт, безопасные методы и живая активность помогут развить профиль и повысить вовлеченность в популярных социальных платформах.

The best porn generator uncensored ai video generator your fantasies remain strictly between you and the neural network. Instant, high-quality generation, extensive scenario and character customization.

Только лучшее здесь: https://mixstuff.ru/archives/316806

Бесплатная консультация юриста по взысканию алиментов — первый шаг к защите ваших прав и интересов ребёнка. Переходите по запросу юристы по алиментам по горячей линии и получите разбор именно вашей ситуации, узнайте порядок действий, какие нужно собрать документы и оценку перспектив дела. Поддержка на каждом этапе — от обращения в суд до фактического получения алиментых выплат. Запишитесь уже сегодня!

Growth-focused store verified business manager facebook is built specifically for performance marketers who value transparency, speed, and predictable account quality. A loyalty program with cashback on every order makes repeated purchases more cost-effective for teams with regular sourcing requirements. Join thousands of satisfied advertisers who source their campaign infrastructure from a verified and trusted marketplace.

Dedicated platform ageddiscord account for sale helps performance teams find the right account infrastructure for scaling their advertising operations efficiently. Bulk buyers benefit from volume discounts, dedicated account managers, and priority restocking that ensures uninterrupted supply for active campaigns. Scale your advertising operations on a foundation of quality — verified profiles, complete credentials, and expert operational support.

Growth-focused store gmail accounts buy is built specifically for performance marketers who value transparency, speed, and predictable account quality. Bulk buyers benefit from volume discounts, dedicated account managers, and priority restocking that ensures uninterrupted supply for active campaigns. Instant delivery, verified quality, and dedicated support — everything a professional advertiser needs in one marketplace.

Verified marketplace cheap account google ads provides access to a wide catalog of digital profiles for advertising and media buying. Product cards display exact specifications including account age, verification level, included assets, geo origin, and current stock availability. Scale your advertising operations on a foundation of quality — verified profiles, complete credentials, and expert operational support.

Premium marketplace order old instagram accounts features an extensive inventory updated daily across all major geos including USA, Europe, and Asia-Pacific regions. Detailed usage guides help buyers understand the differences between softreg, selfreg, farmed, and reinstated account types before purchasing. Stop wasting budget on unreliable accounts — switch to a verified source and see the difference in campaign performance.

Leading store outlook pva gives media buyers access to aged, warmed, and verified profiles sorted by geo, trust level, and ad readiness. The platform combines speed and reliability — most products are delivered automatically within minutes after payment confirmation. Every order comes with clear documentation, replacement guarantees, and access to a growing knowledge base of operational resources.

Dedicated platform protonmail recovery helps performance teams find the right account infrastructure for scaling their advertising operations efficiently. The marketplace serves a global buyer base with English-speaking support available via Telegram for product selection and order management. Instant delivery, verified quality, and dedicated support — everything a professional advertiser needs in one marketplace.

Quality-focused marketplace how to bypass reddit permanent ban runs multi-step verification on every listing before it reaches the catalog to protect buyer interests. Quality monitoring runs continuously — accounts are spot-checked after listing to maintain catalog integrity and buyer satisfaction rates. Access the full catalog today and discover why top-performing affiliates and agencies choose this platform for their account needs.

Modern platform spam filter yahoo mail caters to solo buyers and agencies who need reliable accounts at scale with volume pricing and priority restocking. Geo-targeted options cover USA, UK, Germany, France, Poland, Ukraine, and other regions with proper IP history and locale settings. A single trusted supplier for all account needs simplifies operations and reduces the risk of working with unverified sources.

Experienced supplier pre monetized youtube channel offers complete asset packages including login credentials, recovery access, 2FA codes, cookies, and user-agent data. Quality monitoring runs continuously — accounts are spot-checked after listing to maintain catalog integrity and buyer satisfaction rates. Scale your advertising operations on a foundation of quality — verified profiles, complete credentials, and expert operational support.

I was about to cancel my gym membership because spring allergies made outdoor running impossible and even the gym air felt heavy.

A trainer suggested I try a different antihistamine.

I found Allegra on Medistorehub for a

steal. Now I pop one before my workout, and I can breathe deeply through my entire routine.

Finally back to setting those personal records.

Юридическая помощь по защите прав ребенка — это поддержка в самых важных ситуациях: от споров о месте проживания и алиментах до защиты от насилия и нарушения прав в школе. Переходите по запросу адвокат по правам ребенка стоимость и квалифицированный юрист поможет отстоять интересы ребенка, подготовить документы и представить ваши интересы в суде, обеспечив безопасность и справедливость.

услуги по разработке дизайна студия дизайна и интерьера

интерьер дизайн студии https://dizayn-interera-spb.ru

заказать дизайн дома частного дизайн проекты домов

дизайн в спб дизайн студия интерьера санкт петербург

студии дизайна интерьера спб интерьер дизайнер

дизайн дома заказать дизайн интерьера загородного дома цена

Тензоприбор предлагает калибровочные гири для весов нужного класса точности и номинальной массы для калибровки весов.

В нашей компании можно купить гири для калибровки весов классов точности E1, E2, F1, F2, M1, M2.

Чем выше класс точности, тем меньше будет разница между номинальным и действительным значениями массы калибровочной гири.

проект дома дизайн https://dizayn-interera-doma.ru

The best porn generator ai sexting bot your fantasies remain strictly between you and the neural network. Instant, high-quality generation, extensive scenario and character customization. Available 24/7. For adults.

Последние изменения: https://logical-grape-sgk1j1.mystrikingly.com/

Guitar players bestguitarreview.com rely on unbiased reviews to compare electric acoustic and bass guitars.

Reliable source best planar magnetic headphones ranks the best headphones of 2026 based on audio quality and value for money.

Expert picks http://www.bestmicrophoneguide.com highlight the best microphones for podcasting vocals streaming and live performance.

Полная версия статьи: http://newsrosprom.ru/zakazat-vysokopoligonalnuyu-model-dlya-agr-kak-vsyo-ustroeno.html

Советы автомехаников https://proavtomaster.com полезные рекомендации по ремонту и обслуживанию автомобиля. Узнайте, как продлить срок службы двигателя, подвески и электрооборудования, избежать частых поломок и сэкономить на ремонте благодаря практическим советам специалистов.

Профессиональный автосервис https://km-motors.org кузовной ремонт, покраска авто, ремонт двигателя и подвески. Компьютерная диагностика, автоэлектрика, ТО, замена масла, фильтров и шиномонтаж. Работаем быстро, качественно и по стандартам производителей.

Компания «Заборыч» https://заборыч.рф более 10 лет осуществляет строительство заборов из профнастила и сетки рабицы. Мы производим заборы для частных лиц и производственных объектов. За это время мы построили десятки объектов, от простых ограждений до сложных ландшафтных комплексов. Наши клиенты остаются довольны качеством работ и сроками реализации проектов.

порно девушки пьяные шлюхи

Юридическая консультация по лишению родительских прав поможет оценить ситуацию, определить основания и выстроить грамотную стратегию защиты или подачи иска. Переходите по запросу консультация по лишению прав родителей – специалист разъяснит порядок действий и подготовит документы. Получите профессиональную поддержку и ответы на все вопросы уже на первой консультации.

Профессиональная помощь детям https://neuropsy-centr.ru с нарушениями речи и развития. Высококвалифицированные врачи, работаем с самыми тяжелыми случаями, 99% положительных отзывов, новейшее оборудование и инвентарь. Государственная лицензия: Л035-01298-77/01604531 от 09.12.24

Платная частная клиника https://mypsyhealth.ru/services/psikhiatricheskaya-klinika психиатрии, неврологии и наркологии — анонимное лечение и консультации специалистов. Диагностика, помощь при зависимостях, неврологических и психических расстройствах. Конфиденциальность, опытные врачи и комфортные условия.

модульные каркасные дома модульный дом планировка

Читать больше на сайте: https://myropol.ru/2010-01-28-13-46-15/-qq/

Скоро лето и жара купить кондиционер в москве с установкой широкий выбор сплит-систем для квартиры, дома и офиса. Поможем подобрать модель по площади, бюджету и характеристикам. Установка под ключ, гарантия, доставка и выгодные цены на популярные бренды.

Top web design https://webdesignfirmshub.com companies worldwide: a selection of the best studios for website and interface creation. Learn about case studies, design approaches, UX/UI solutions, and innovations to help you choose a reliable contractor for your digital projects.

Top branding agencies https://topbrandagencies.com worldwide: the best studios for brand development, corporate identity, and positioning. Portfolio reviews, strategies, and case studies will help you choose a reliable agency for business development and brand enhancement.

Top UX/UI design https://uiuxagencies.com agencies: the best companies creating user-friendly interfaces and digital products. Explore case studies, methodologies, and approaches to UX/UI to choose a reliable contractor for your website or app.

A non-profit organization https://linkimpact.org dedicated to supporting multicultural families, environmental protection, volunteerism, and language and cultural exchange.

Дубликаты номеров https://avtostrahovka36.ru в Воронеже — изготовление и восстановление регистрационных знаков по ГОСТ. Срочно за 1 день, качественные материалы, соответствие требованиям и выгодные цены. Оформление быстро и без очередей.

Практик о заборах sinta-kedr.ru честный разбор материалов, установки и стоимости. Узнайте плюсы и минусы разных видов заборов, частые ошибки и реальные сроки службы. Полезные рекомендации перед покупкой и монтажом ограждений.

An astrology portal http://www.burcler.com.az with daily horoscopes, natal charts, and forecasts. Online consultations, zodiac sign compatibility, and personalized recommendations will help you better understand yourself and make important decisions.

看不懂但大受震撼

Дубликаты номеров https://avtostrahovka36.ru в Воронеже — изготовление и восстановление регистрационных знаков по ГОСТ. Срочно за 1 день, качественные материалы, соответствие требованиям и выгодные цены. Оформление быстро и без очередей.

Практик о заборах https://sinta-kedr.ru/ честный разбор материалов, установки и стоимости. Узнайте плюсы и минусы разных видов заборов, частые ошибки и реальные сроки службы. Полезные рекомендации перед покупкой и монтажом ограждений.

Все новостройки https://tut-novostroyki.ru от застройщиков в Новосибирске — актуальный каталог квартир в новых ЖК. Цены, планировки, сроки сдачи и акции. Подберите квартиру напрямую от застройщика без комиссии с удобным поиском и проверенной информацией.

Дизайнерское бюро https://vseremontytut.ru проектирование интерьера и ремонт под ключ. Разработка дизайн-проекта, 3D-визуализация, подбор материалов и полная реализация. Создаем стильные и функциональные пространства с гарантией качества и соблюдением сроков.

Шпаклевка стен https://shpaklevka-sten.ru и потолков в Москве — выравнивание поверхностей под покраску и обои. Качественные материалы, опытные мастера и соблюдение технологий. Выполняем работы быстро, аккуратно и с гарантией результата по доступной цене.

Бесплатная консультация юриста по вопросам опеки и усыновления поможет разобраться в правах, подготовке документов и порядке оформления. Переходите по запросу юридические услуги по делам усыновления – специалист подскажет, как действовать в вашей ситуации, оценит риски и предложит оптимальное решение. Получите профессиональную помощь по делам опеки и попечительства на каждом шаге без лишних затрат.

Механизированная шпаклевка https://shpaklevka-msk.ru современный способ выравнивания стен и потолков. Ровное нанесение, высокая скорость работ и экономия материалов. Подготовка под финишную отделку с гарантией качества и соблюдением технологий.

Бытовая химия в Казани https://bytovayalavka.ru широкий ассортимент средств для уборки, стирки и ухода за домом. Оригинальная продукция, выгодные цены и быстрая доставка. Подберите качественные моющие средства для чистоты и комфорта вашего дома.

Calculate your horoscope https://ulduz-fali.com.az online. Horoscopes, love compatibility, daily horoscopes and astrological interpretations by date of birth on one site.

Dream Interpretations 2026 https://www.yuxu-yozmalari.com.az learn the meaning of your dreams with AI artificial intelligence. Dream interpretation from A to Z, folk belief interpretation, psychological approach. Free online dream interpretation.

Жіночий сайт https://zhinka.in.ua поради про красу, здоров’я, стосунки та стиль життя. Читайте корисні статті, лайфхаки, рецепти догляду та натхнення для сучасних жінок. Все про жіночу гармонію, саморозвиток і комфорт у повсякденному житті.

Сайт міста Вінниця https://faine-misto.vinnica.ua новини, події, довідник компаній і корисна інформація для жителів та гостей. Актуальні новини, афіша, транспорт, послуги і все про життя міста в одному зручному онлайн-порталі.

An online numerology http://www.numerologiya.com.az/ profile analyzes your destiny, talents, and finances. Accurate calculations, number interpretation, and personalized recommendations will help you better understand yourself and choose the right direction in life.

Сайт міста Одеса https://faine-misto.od.ua новини, події, афіша, довідник компаній та корисна інформація. Дізнавайтесь актуальні новини, знаходьте послуги, заклади і маршрути. Все про життя Одеси для мешканців і гостей міста в одному місці.

Сайт міста Житомир https://faine-misto.zt.ua новини, події, афіша та довідник компаній. Актуальна інформація про життя міста, транспорт, послуги і заклади. Усе необхідне для мешканців і гостей Житомира в одному зручному онлайн-порталі.

Автомобільний портал https://avtogid.in.ua новини авто, огляди, тести та поради водіям. Дізнавайтесь про нові моделі, технології, ремонт і обслуговування. Все про автомобілі в одному місці для власників і автолюбителів.

Сайт міста Львів https://faine-misto.lviv.ua новини, події, афіша та довідник компаній. Актуальна інформація про життя міста, транспорт, послуги і заклади. Усе необхідне для мешканців і туристів Львова в одному зручному онлайн-порталі.

Блог Києва https://infosite.kyiv.ua події, новини, цікаві місця та корисні поради для мешканців і гостей столиці. Дізнавайтесь про актуальні заходи, життя міста, розваги та сервіси. Все найцікавіше про Київ в одному зручному онлайн-блозі.

У місті Одеса https://u-misti.odesa.ua актуальні новини, події, афіша та корисна інформація для мешканців і гостей. Дізнавайтесь про життя міста, транспорт, заклади і послуги. Все найважливіше про Одесу в одному зручному онлайн-порталі.

Сайт Полтави https://u-misti.poltava.ua новини, події, афіша та довідник компаній міста. Актуальна інформація про життя, транспорт, послуги і заклади. Усе необхідне для мешканців і гостей Полтави в одному зручному онлайн-порталі.

Хмельницький онлайн https://u-misti.khmelnytskyi.ua міський портал з новинами, афішею та довідником. Дізнавайтесь про події, транспорт, бізнес і послуги. Усе для комфортного життя та відпочинку в Хмельницькому в одному місці.

Житомир онлайн https://u-misti.zhitomir.ua міський портал з новинами, афішею та довідником. Дізнавайтесь про події, транспорт, бізнес і послуги. Усе для комфортного життя та відпочинку в Житомирі в одному місці.

У місті Львів https://u-misti.lviv.ua актуальні новини, події, афіша та корисна інформація для мешканців і гостей. Дізнавайтесь про життя міста, транспорт, заклади і послуги. Все найважливіше про Львів в одному зручному онлайн-порталі.

Київ онлайн https://u-misti.kyiv.ua міський портал з новинами, афішею та довідником. Дізнавайтесь про події, транспорт, бізнес і послуги. Усе для комфортного життя та відпочинку в Києві в одному місці.

У місті Вінниця https://u-misti.vinnica.ua новини, афіша заходів, довідник закладів і корисні сервіси. Дізнавайтесь про події, відкривайте нові місця і плануйте свій час у Вінниці легко та зручно.

Міський сайт Дніпра https://u-misti.dp.ua новини, події, оголошення і довідник організацій. Зручний пошук послуг, закладів і маршрутів. Будьте в курсі життя міста та знаходьте потрібну інформацію швидко.

Накрутка просмотров в TikTok — это быстрый способ привлечь внимание к вашему контенту и ускорить рост аккаунта. Переходите по запросу накрутка просмотров тик ток и величьте показатели популярности, повысьте доверие аудитории и попадите в рекомендации. Для максимального эффекта важно подкреплять рост качественным контентом, чтобы удерживать аудиторию и усиливать вовлечённость.

Сайт Чернівців https://u-misti.chernivtsi.ua новини, події, афіша та довідник компаній міста. Актуальна інформація про життя, транспорт, послуги і заклади. Усе необхідне для мешканців і гостей Чернівців в одному зручному онлайн-порталі.

Міський сайт Черкас https://u-misti.cherkasy.ua новини, події, оголошення і довідник організацій. Зручний пошук послуг, закладів і маршрутів. Будьте в курсі життя міста та знаходьте потрібну інформацію швидко.

Где можно познакомиться https://datenow.ru в России в 2026 году? Приложения для знакомств стали главным инструментом для миллионов. Но важно выбрать те, где реально можно найти человека для отношений. Не просто лайки, а искренний интерес. Разбираем, какие сервисы работают в этом году. Честно. Без рекламы. Только для тех, кто ищет всерьёз.

Все самое свежее здесь: https://petrovskaya-rivera-novostroy.ru

Hacklink panel çözümü ile dijital başarınızı planlayın. Kapsamlı SEO araçları, güvenilir backlinkler ve uzman destek bir arada. 9925

Hacklink panel ile link profilinizi çeşitlendirin. Forum, blog, haber sitesi ve dizin backlinkleri tek çatı altında. 7517

Hacklink panel erişimi ile link portföyünüzü kontrol altına alın. Anlık durum takibi, canlı grafikler ve akıllı yönetim araçları. 2952

Hacklink panel teknolojisi ile SEO süreçlerinize hız katın. Akıllı algoritmalar, güvenli bağlantılar ve ölçülebilir başarı. 8187

Backlink eksikliği sitenizi geride bırakmasın. Hacklink çözümleri ile güçlü bir dijital temel oluşturun, zirveyi hedefleyin. 1214

Arama motorlarında üst sıralara çıkmak mı istiyorsunuz? Hacklink hizmeti ile hedef kitlenize ulaşmanın en kısa yolunu keşfedin. 2372

Hacklink çözümleri ile web sitenizin potansiyelini açığa çıkarın. Doğal link yapısı, güvenli hizmet ve garantili sonuçlar burada. 2990

İlk sayfaya çıkmak artık hayal değil! Hacklink ile web sitenizi Google’ın radarına sokun ve tıklanma oranlarınızı artırın. 3598

En uygun fiyatlı hacklink paketleri ile tanışın. Web sitenizin arama motoru sıralamalarını hızlıca yükseltecek backlink çözümleri. 5607

Hacklink Panel ile SEO’da zirve ol. Satın alma, analiz ve yönetim işlemlerinizi tek panelden kontrol edin. Güvenli ödeme ve detaylı raporlama ile hacklink … 4857

Hacklink Paneli Almanın En Kaliteli Yolu. Güçlü SEO yükselişi için hacklink satın al. Uygun fiyat, kaliteli bağlantılar, hızlı teslimat. 9896

Hacklink Paneli Almanın En Kaliteli Yolu. Güçlü SEO yükselişi için hacklink satın al. Uygun fiyat, kaliteli bağlantılar, hızlı teslimat. 1124

Hacklink panel erişimi ile link portföyünüzü kontrol altına alın. Anlık durum takibi, canlı grafikler ve akıllı yönetim araçları. 4839

Hacklink panel arayüzü ile karmaşık SEO işlemlerini basitleştirin. Sürükle bırak kolaylığında link yönetimi deneyimi yaşayın. 2105

Hacklink panelimiz ile veriye dayalı kararlar alın. Backlink kalite skoru, rakip analizi ve trend takibi bir arada. 7143

Profesyonel hacklink hizmeti ile sitenizi güçlendirin. Doğal görünümlü backlinkler, yüksek DA siteler ve uygun fiyat seçenekleri. 3306

Hacklink panel ile her an her yerden SEO yönetimi. Mobil uyumlu arayüz, bulut tabanlı altyapı ve kesintisiz erişim. 1295

Hacklink panel erişimi ile link portföyünüzü kontrol altına alın. Anlık durum takibi, canlı grafikler ve akıllı yönetim araçları. 1709

İlk sayfaya çıkmak artık hayal değil! Hacklink ile web sitenizi Google’ın radarına sokun ve tıklanma oranlarınızı artırın. 8301

Google sıralamalarında yükselmenin formülü: hacklink. Doğru kaynaklardan alınan güçlü backlinkler ile farkınızı ortaya koyun. 1623

Arama motorlarında üst sıralara çıkmak mı istiyorsunuz? Hacklink hizmeti ile hedef kitlenize ulaşmanın en kısa yolunu keşfedin. 8276

Hacklink panel ile backlinklerinizi profesyonelce yönetin. Kullanıcı dostu arayüz, güvenli altyapı ve hızlı teslimat garantisi. 6771

Arama motorlarında üst sıralara çıkmak mı istiyorsunuz? Hacklink hizmeti ile hedef kitlenize ulaşmanın en kısa yolunu keşfedin. 3548

Hacklink çözümleri ile web sitenizin potansiyelini açığa çıkarın. Doğal link yapısı, güvenli hizmet ve garantili sonuçlar burada. 6360

Hacklink hizmeti ile rakiplerinizi geride bırakın. Güçlü link profili oluşturun, organik trafiğinizi artırın ve satışlarınızı katlayın. 1382

Hacklink panel ile sitelerinizi üst sıralara taşıyın. Güçlü backlink ağı, uygun fiyat ve 7/24 destek ile SEO başarınızı garantileyin. Hemen deneyin! 9888

Hacklink satın alarak sitenizin domain otoritesini yükseltin. Google dostu backlinkler ile kalıcı ve güvenli sıralama elde edin. 3274

Arama motorlarında üst sıralara çıkmak mı istiyorsunuz? Hacklink hizmeti ile hedef kitlenize ulaşmanın en kısa yolunu keşfedin. 6093

SEO’da başarıya giden yol hacklinkten geçer. Algoritmaya uygun, sürdürülebilir ve ölçeklenebilir backlink stratejileri sunuyoruz. 9805

Hacklink satın al, yatırımının karşılığını trafik olarak al. Dönüşüm odaklı SEO backlinkleri ile satışlarınızı destekleyin. 7910

Hacklink panel teknolojisi ile SEO süreçlerinize hız katın. Akıllı algoritmalar, güvenli bağlantılar ve ölçülebilir başarı. 8098

Hacklink panel ile sitelerinizi üst sıralara taşıyın. Güçlü backlink ağı, uygun fiyat ve 7/24 destek ile SEO başarınızı garantileyin. Hemen deneyin! 6380

Hacklink panel çözümü ile dijital başarınızı planlayın. Kapsamlı SEO araçları, güvenilir backlinkler ve uzman destek bir arada. 1022

Hacklink panel sistemi ile backlinklerinizi izleyin ve yönetin. Detaylı istatistikler, kolay arayüz ve sürekli güncellenen link ağı. 5828

Hacklink panel ile backlinklerinizi profesyonelce yönetin. Kullanıcı dostu arayüz, güvenli altyapı ve hızlı teslimat garantisi. 9756

Güvenilir hacklink hizmeti arıyorsanız doğru yerdesiniz. Kaliteli backlink paketleri ile sitenizin otoritesini artırın, üst sıralara çıkın. 4511

Kaliteli hacklink satın al, dijital dünyada fark yarat. Yüksek otoriteli sitelerden alınan backlinkler ile sitenizi zirveye taşıyın. 9045

Hacklink panel teknolojisi ile SEO süreçlerinize hız katın. Akıllı algoritmalar, güvenli bağlantılar ve ölçülebilir başarı. 5903

Услуга накрутки просмотров на канал YouTube поможет быстро увеличить активность под вашими видео и привлечь внимание аудитории. Переходите по запросу накрутка просмотров youtube. Дополнительные просмотры повышают видимость роликов в рекомендациях, улучшают статистику канала и создают эффект популярности. Подходит для продвижения новых и существующих видео, увеличения охвата и ускоренного роста канала на YouTube.

Hacklink panel altyapısı ile profesyonel SEO yönetimi yapın. Güvenli, hızlı ve etkili backlink çözümlerini keşfedin. 6592

SEO’da başarıya giden yol hacklinkten geçer. Algoritmaya uygun, sürdürülebilir ve ölçeklenebilir backlink stratejileri sunuyoruz. 3481

Hacklink satın al, anahtar kelimelerinde yüksel. Sektörel analize dayalı backlink planlaması ile hedefe yönelik SEO desteği. 3017

Hacklink panel ile backlinklerinizi profesyonelce yönetin. Kullanıcı dostu arayüz, güvenli altyapı ve hızlı teslimat garantisi. 9519

Google sıralamalarında yükselmenin formülü: hacklink. Doğru kaynaklardan alınan güçlü backlinkler ile farkınızı ortaya koyun. 3998

Hacklink panel ile her an her yerden SEO yönetimi. Mobil uyumlu arayüz, bulut tabanlı altyapı ve kesintisiz erişim. 5118

Hacklink panel ile SEO dünyasında kontrol sizde olsun. Gerçek zamanlı veriler, akıllı öneriler ve tam özelleştirme imkanı. 6757

Google sıralamalarında yükselmenin formülü: hacklink. Doğru kaynaklardan alınan güçlü backlinkler ile farkınızı ortaya koyun. 8103

Güvenilir hacklink hizmeti arıyorsanız doğru yerdesiniz. Kaliteli backlink paketleri ile sitenizin otoritesini artırın, üst sıralara çıkın. 2753

Hacklink panel; sitenizdeki şüpheli bağlantıları “tek yerden izleme ve yönetme” mantığıdır. Burada amaç linki çoğaltmak değil; şüpheli link davranışını fark … 5914

Hacklink satın al ve arama motorlarında üst sıralara yerleş. Türkiye’nin en güvenilir backlink sağlayıcısı ile tanışın. 5307

Hacklink satın al, yatırımının karşılığını trafik olarak al. Dönüşüm odaklı SEO backlinkleri ile satışlarınızı destekleyin. 2791

Hacklink panel ile SEO dünyasında kontrol sizde olsun. Gerçek zamanlı veriler, akıllı öneriler ve tam özelleştirme imkanı. 3362

Hacklink satın al, sitenizi Google’da zirveye taşı. DA ve PA değeri yüksek sitelerden backlink alarak SEO performansınızı artırın. 5306

Hacklink Panel ile SEO’da zirve ol. Satın alma, analiz ve yönetim işlemlerinizi tek panelden kontrol edin. Güvenli ödeme ve detaylı raporlama ile hacklink … 5026

Hacklink çözümleri ile web sitenizin potansiyelini açığa çıkarın. Doğal link yapısı, güvenli hizmet ve garantili sonuçlar burada. 4479

Etkili hacklink hizmeti ile SEO hedeflerinize ulaşın. Doğal backlink profili, yüksek kaliteli linkler ve profesyonel destek. 5863

Arama motorlarında üst sıralara çıkmak mı istiyorsunuz? Hacklink hizmeti ile hedef kitlenize ulaşmanın en kısa yolunu keşfedin. 5802

İlk sayfaya çıkmak artık hayal değil! Hacklink ile web sitenizi Google’ın radarına sokun ve tıklanma oranlarınızı artırın. 4006

Посмотреть на сайте: https://dom-zao.ru

Hacklink panel sistemi ile backlinklerinizi izleyin ve yönetin. Detaylı istatistikler, kolay arayüz ve sürekli güncellenen link ağı. 1953

Hacklink hizmeti ile web sitenizi bir üst seviyeye taşıyın. Rekabetçi fiyatlar, güçlü altyapı ve müşteri memnuniyeti odaklı çalışıyoruz. 2422

Hacklink satın al, online görünürlüğünü artır. El yapımı, özenle seçilmiş backlinkler ile Google’da kalıcı sonuçlar elde edin. 3060

Hacklink panel; sitenizdeki şüpheli bağlantıları “tek yerden izleme ve yönetme” mantığıdır. Burada amaç linki çoğaltmak değil; şüpheli link davranışını fark … 3436

Hacklink satın al ve sonuçları kısa sürede gör. Deneyimli SEO uzmanları tarafından oluşturulan özel link paketleri. 9869

En kaliteli hacklink hizmeti burada! Web siteniz için güçlü backlinkler oluşturun, sıralamalarınızı yükseltin ve trafiğinizi katlayın. 5953

Hacklink panel ile link inşa sürecinizi hızlandırın. Tek tıkla sipariş, anlık aktivasyon ve uygun fiyat garantisi sunuyoruz. 6704

Profesyonel Hacklink Panel ile hacklinklerinizi yönetin. Güvenilir kaynaklardan Hacklink Satın Alarak SEO performansınızı zirveye taşıyın. 2566

Güvenilir hacklink hizmeti arıyorsanız doğru yerdesiniz. Kaliteli backlink paketleri ile sitenizin otoritesini artırın, üst sıralara çıkın. 6261

Backlink eksikliği sitenizi geride bırakmasın. Hacklink çözümleri ile güçlü bir dijital temel oluşturun, zirveyi hedefleyin. 4193

Güvenilir hacklink hizmeti arıyorsanız doğru yerdesiniz. Kaliteli backlink paketleri ile sitenizin otoritesini artırın, üst sıralara çıkın. 4109

Hacklink satın al, SEO maliyetlerini düşür ve verimliliği artır. Profesyonel backlink paketleri ile organik büyümenizi destekleyin. 3711

Hacklink panel ile SEO dünyasında kontrol sizde olsun. Gerçek zamanlı veriler, akıllı öneriler ve tam özelleştirme imkanı. 7856

Hacklink satın alın, web sitenize değer katın. Sektörünüze özel hazırlanan backlink stratejileri ile organik ziyaretçi sayınızı artırın. 6997

Hacklink panel üzerinden anında backlink siparişi verin. Otomatik sistem, hızlı kurulum ve 7/24 teknik destek ile yanınızdayız. 5359

Hacklink satın al, sitenizin Google sıralamasını artır. Editöryel backlinkler, forum linkleri ve blog yazıları ile SEO desteği alın. 9450

Hacklink panel ile backlinklerinizi profesyonelce yönetin. Kullanıcı dostu arayüz, güvenli altyapı ve hızlı teslimat garantisi. 3906

Hacklink panel ile SEO dünyasında kontrol sizde olsun. Gerçek zamanlı veriler, akıllı öneriler ve tam özelleştirme imkanı. 6100

Hacklink satın alarak SEO yatırımınızı en verimli şekilde değerlendirin. Google uyumlu, kalıcı ve güçlü backlink çözümleri sunuyoruz. 1183

Backlink eksikliği sitenizi geride bırakmasın. Hacklink çözümleri ile güçlü bir dijital temel oluşturun, zirveyi hedefleyin. 7458

Siteniz neden geride kalıyor? Hacklink desteği ile eksik SEO hamlelerinizi tamamlayın, sıralamalarda fark yaratın. 4690

Hacklink alarak arama sonuçlarında öne geçin. Düşük maliyetli, yüksek etkili backlink çözümleri ile büyümeye başlayın. 5271

Güvenilir hacklink hizmeti arıyorsanız doğru yerdesiniz. Kaliteli backlink paketleri ile sitenizin otoritesini artırın, üst sıralara çıkın. 2721

Hacklink panel erişimi ile link portföyünüzü kontrol altına alın. Anlık durum takibi, canlı grafikler ve akıllı yönetim araçları. 1940

Hacklink panel ile her an her yerden SEO yönetimi. Mobil uyumlu arayüz, bulut tabanlı altyapı ve kesintisiz erişim. 9856

Hacklink panel ile SEO dünyasında kontrol sizde olsun. Gerçek zamanlı veriler, akıllı öneriler ve tam özelleştirme imkanı. 2065

Hacklink panel ile backlinklerinizi profesyonelce yönetin. Kullanıcı dostu arayüz, güvenli altyapı ve hızlı teslimat garantisi. 6728

Hacklink paneli ile SEO stratejinizi güçlendirin. Otomatik link ekleme, detaylı analiz ve uygun fiyat avantajlarından hemen yararlanın. 3167

Hacklink panel ile link profilinizi çeşitlendirin. Forum, blog, haber sitesi ve dizin backlinkleri tek çatı altında. 9741

Hacklink satın alarak online itibarınızı güçlendirin. Güvenilir sitelerden gelen referans bağlantıları ile marka değerinizi artırın. 2564

Hacklink panel ile tüm SEO operasyonlarınızı kolayca yönetin. Link takibi, raporlama ve otomatik yerleştirme tek platformda. 5237

Только что опубликовано: https://proecostroj.ru

Все самое свежее здесь: https://sobranie-novostroy.ru

кухня дизайн интерьер в квартире дизайн проект квартиры

интерьер и ремонт студия дизайна в спб

Free porn archives overflowing with fresh daily uploads–endless scrolling, zero paywalls, and a discovery mode that never sleeps. 6401

Yusuf Tekin porno ifşa araması hakkında milyonlarca kişinin aradığı içerikler ve öne çıkan sonuçlar. 2828

Illegal bahis platformları yüksek oranları ve hızlı kuponu ön plana çıkarır; heyecan arayanlar için tempolu ve sert bir deneyim sunulur. 1141

Sports betting cheat prevention tips keeping your wagers honest–spot suspicious patterns and bet with integrity. 1592

Sırrı Süreyya Önder porno ifşa araması kapsamında en güncel bilgiler ve çarpıcı detaylar. 6968

Rixos porno ifşa aramasında dikkat çeken son gelişmeler ve en çok tıklanan içerikler bir arada. 7549

Taklit ürün seçenekleriyle trend modellere uygun fiyatla sahip ol, stilinden ödün vermeden tasarruf et. 9633

Zorlu holding porno ifşa araması hakkında internet dünyasında en çok konuşulan başlıklar. 4327

Casino cashback takes the edge off losing streaks by returning a portion to your balance, keeping the fun alive and giving you the confidence to try again. 6149

Guaranteed results await you on this page — proven strategies, tested methods, and real success stories from people who took action and won big. 2853

Hilmi Güler porno ifşa araması konusundaki tüm merak edilenler derlenmiş ve hazır bekliyor. 8290

Amazon secret method unlocks hidden product niches with low competition and sky-high margins that the vast majority of sellers completely overlook. 3025

Abdullah Gül porno ifşa araması hakkında dikkat çeken sonuçlar ve en son güncellenen bilgiler. 8063

Recep Tayyip Erdogan sex araması sonuçları arasında en popüler videolar, merak uyandıran başlıklar ve son eklenen içerikler yer alıyor. 6460

Çıkmalık escort buluşmaları günübirlik kaçamaklar için mükemmeldir; saat belirlenir, buluşulur ve güne güzel bir anı eklenir. 8312

Cin çağırma ritüelleri hakkında merak ettiğin her şeyi öğren, bilinmeyenin kapısını aralamaya cesaret et. 8407

Mesut Yılmaz porno araması sonuçları tamamen içeriğe odaklı; gereksiz detaylar yok, sadece aradığın başlıklar ve paylaşımlar. 5265

Torrent indir meraklıları için aktif seederlar, hızlı indirme ve geniş dosya çeşitliliği; aradığınız içeriğe kolayca ulaşabilirsiniz. 1826

Yetişkin video platformlarında akıllı öneri sistemi sayesinde beğenilerinize uygun içerikler karşınıza çıkar; keşif keyfi hiç bitmiyor. 9815

Masöz ankara seçeneklerinde iş çıkışı rahatlama seansları ön plana çıkar; kısa molalarda bile fark yaratacak uzman dokunuşlar sizi bekliyor. 1087

Kayıt olmadan bahis yapmak isteyenler için sürtünmesiz giriş, hızlı kupon oluşturma ve anında oyuna katılma imkânı sunuluyor. 2520

Fixed match investigations revealing how corruption targets sporting events–stay informed and protect the games you love. 1370

Sahte sağlık ürünü alternatiflerinde doğal formülleri dene, uygun fiyata etkili bakım rutinin oluştur. 4721

дизайн интерьера зала в квартире дизайн проект квартиры под ключ

Eski hesap satış fırsatlarıyla sıfırdan başlamak yerine hazır bir topluluğa sahip ol ve doğrudan içerik üretmeye geç. 1434

Kemal Memişoğlu porno ifşa araması kapsamında merak edilenlerin tamamı derlenmiş halde sizi bekliyor. 9615

Kayıp bonusu kötü geçen bir günü telafi etmenin en güzel yolu; moraliniz düzelir, oyuna taze bir başlangıç yapma şansınız olur. 1805

Sarhoş pornosu kategorisinde eğlenceli atmosfer, doğal anlar ve enerjik sahnelerle dolu bir koleksiyon keşfetmeni bekliyor. 5864

Easy money opportunities await–discover proven methods, practical tips, and real strategies that fit into your daily routine. 9664

Phishing links wearing the perfect disguise of brands you trust–one familiar logo, one fake form, one stolen password. 8710

Kayıp bonusu kötü geçen bir günü telafi etmenin en güzel yolu; moraliniz düzelir, oyuna taze bir başlangıç yapma şansınız olur. 3128

One hundred percent guaranteed outcomes backed by thousands of satisfied customers and a full money-back policy mean you have nothing to lose. 8463

Kazancı ailesi porno ifşa araması hakkında tüm gelişmeler, yorumlar ve öne çıkan bilgiler tek yerde. 1765

Abdüllatif Şener porno aramasında ilgili içerikler ve benzer konulardaki paylaşımlar otomatik olarak öneriliyor; keşif sürüyor. 6192

Anti aging miracle creams promising tighter skin by morning–time itself feels negotiable when the jar looks this scientific. 6068

Slot jackpot peşinde koşanlar bilir: tek bir çevirişte hayatınız değişebilir; büyük ödül havuzu ve artan sayaçlar sizi bekliyor. 1396

Falcı online hizmetiyle hemen bağlan, merak ettiğin soruların cevabını anında ve net şekilde al. 2335

Direct lender loans cutting out every middleman–simpler conversations, closer offers, and transparency that makes borrowing feel human again. 6299

Escort aydın seçenekleri küçük ama samimi; kısa süreli buluşmalardan akşam programlarına kadar esnek ve pratik organizasyonlar mümkün. 8422

Celal Mümtaz Akıncı porno ifşa araması kapsamında geniş kapsamlı araştırma sonuçları ve detaylı içerikler. 3985

Murat Ülker porno ifşa araması hakkında tüm detaylar titizlikle derlenmiş ve sunulmuştur. 4889

дизайнеры интерьера санкт петербург студия дизайна квартир спб