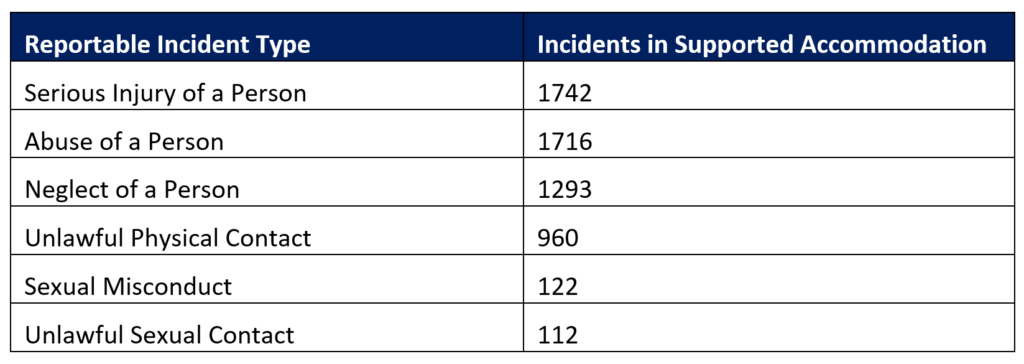

QSC’s Own Motion part 1: how safe is Supported Independent Living?

Examining 6,269 reportable incidents across 7 major providers and 1075 SIL sites, the study represents a significant portion of the SIL cohort, as the selected providers account for 18% of the total. The report suggests that although it is unlikely to lead to the “abolishment” of group homes, there are serious issues that must be addressed.

It’s not easy being a big SIL provider

It’s been a tough year for major providers. Unfortunately, they’re on the wrong end of a confluence of impacts. This means that transformation efforts are complicated because, in most cases, nearly all business functions are impacted by the NDIS cost model.

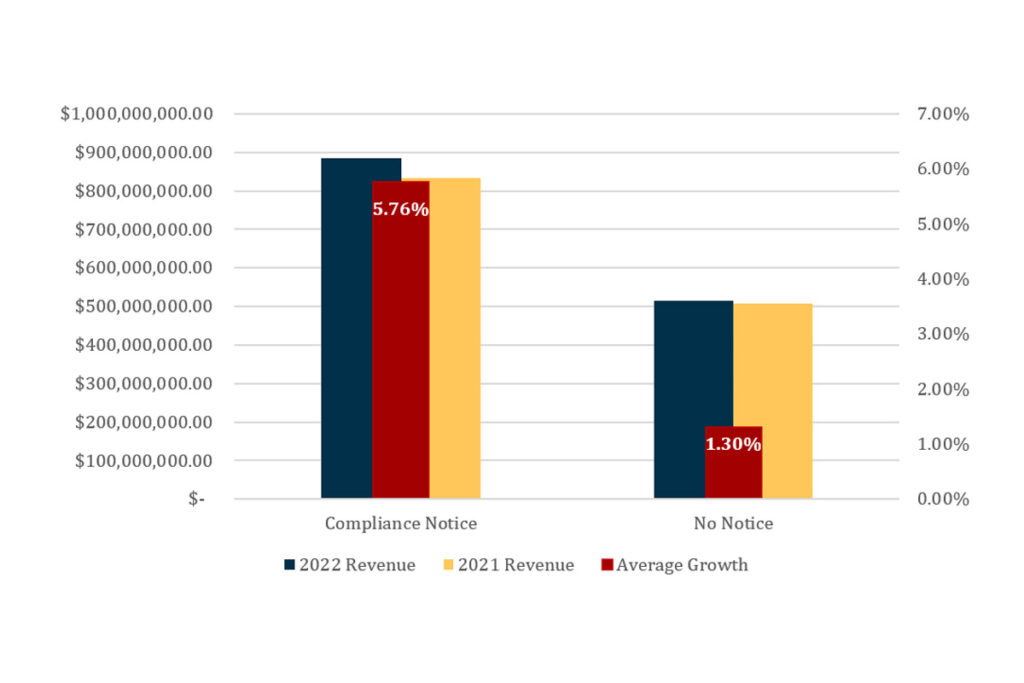

How can a QSC compliance notice lead to growth?

n most markets, we expect government enforcement actions to present serious risks and challenges to businesses. But, unsurprisingly and concerningly, this does not appear to be the case in the NDIS.

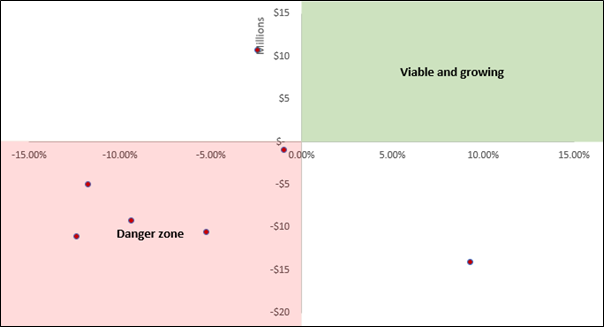

Board members of NDIS providers need to see these 2022 results

Three NDIS providers reported a combined loss of $15 million, with only one posting a minuscule 0.78% margin. These results are a far cry from the exorbitant profits we’ve seen in the media recently.

Our take on disability employment data and theField.jobs

Disability employment has re-entered the spotlight recently with an enquiry into Disability Employment Services (DES) as part of the Disability Royal Commission, along with the launch of a promising new disability-focused jobs website, the Field, co-founded by Dylan Alcott and funded by the Department of Social Services.

Is it getting harder to fill SIL vacancies?

We keep hearing across the sector that filling Supported Independent Living (SIL) vacancies is becoming increasingly more difficult for providers. As always, we reviewed the NDIS data to validate this assumption, and this is what we found.

Why NDIS product strategy is almost always wrong

Let’s say your SIL business is entering the Sydney market for the first time. You will need certain inclusions, such as a robust incident management process. This process is a high-weight critical system required to perform the service. However, it is also low-variance because it varries little between competitors. Therefore, it can not serve as a point of difference. We call these inclusions table stakes.

De-platforming and decentralising to save the disability workforce

As with all attendant care matters in the NDIS, career progression is heavily constrained by the cost model.

A closer look at SIL profitability in 2022

Supported Independent Living (SIL) profitability varies significantly between providers. While many in the NDIS assume that most providers converge on margins of only 2% given the cost model, our data tells us the average margin SIL margin was 4.5%, with considerable variance (3.15% SD).

ILO works, customers want it, so why aren’t we offering it?

Many in the NDIS have considered Individualised Living Options (ILO) as the source of community integration that the scheme initially promised.

However, the data continues to demonstrate that ILO still represents a vanishingly small amount of accommodation payments, and the growth is limited in both a rate and absolute sense. In this article, we review the ILO market from a data-driven perspective.